cfc-news

July 5, 2022

Renewable Capacity Additions Forecast To Rise

Despite suffering from supply chain constraints, increased component shipping costs and rising prices for key commodities, the installation of renewable energy capacity remained at an all-time high in 2021, and capacity is expected to continue climbing this year.

“Many cities, states and utilities have set ambitious clean energy goals and are enacting energy storage procurement mandates,” Jan Ahlen, CFC’s vice president of Utility Research and Policy, said. “Additionally, support for environmental, social and governance (ESG) considerations continues to grow, and demand for cleaner energy sources from corporations is accelerating.”

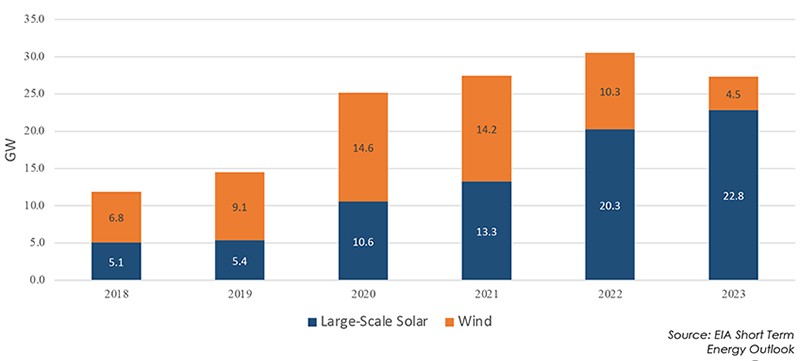

This has led to strong developer interest in solar, wind and battery storage projects, and the U.S. Energy Information Administration (EIA) expects additions to solar and battery capacity will account for more than half of all new electric sector capacity additions in 2022 and 2023.

Wind capacity additions are forecast to total 11 gigawatts (GW) in 2022 and 5 GW in 2023. Utility-scale solar capacity additions are forecast to total 20 GW in 2022 and 22 GW in 2023. In addition, small-scale solar additions (systems less than 1 megawatt) are expected to grow by 6 GW in 2022 and 7 GW in 2023.

Growth of Hybrid Plants

With falling battery prices, there has been a surge of interest in “hybrid” power plants that typically combine generating capacity with co-located batteries.

At least 285 GW of solar capacity that has applied for connection to the grid is proposed as a hybrid plant (42 percent of all planned solar capacity), as is 19 GW of wind capacity (8 percent of planned wind capacity). Additionally, about half of all planned storage capacity (208 GW) is proposed in hybrid configuration.

It is likely that many of these proposed projects will never enter service, however, since most projects that apply for grid interconnection are ultimately withdrawn.

“This situation is not something new,” Ahlen said. “Looking at recent history, only about 23 percent of projects that requested grid interconnection from 2000 to 2016 reached commercial operation. Completion percentages are even lower for wind and solar than other resources. More recently, the total capacity being added to the queues has been growing year-over-year due to higher demand for hybrid systems.”

Even those projects that ultimately are put into service are taking longer, on average, to complete the required studies to become operational. Delays are also sometimes caused by factors outside of the interconnection process, such as securing local permitting or offtake agreements for the power produced.

“Entering an interconnection queue is only the first step in the development process,” Ahlen explained. “Projects also need to have agreements in place with local communities and other stakeholders and may face transmission upgrade requirements.”

In part due to these delays, as well as supply chain challenges, higher material costs and other price inflation and government policy uncertainty, EIA is forecasting an overall slowdown in renewable capacity additions in 2023, primarily wind projects.

Slowdown Ahead?

Supply chain challenges, including bottlenecks at component suppliers, are limiting developers’ ability to procure transformers and transmission equipment, most of which is imported.

Price inflation is also a problem, with shipping rates from China 285 percent higher than levels seen at the beginning of 2020. “These costs are being passed through to prices, influencing inflation,” Ahlen said.

Additionally, there are some unresolved government policy issues that are causing uncertainty among project developers, including the fact that proposed long-term tax incentive extensions for renewable technologies have not yet been approved by Congress.

Finally, last March the U.S. Commerce Department began a review that could enact new tariffs on solar panels and solar cells from Thailand, Malaysia, Cambodia and Vietnam. After clean energy associations warned that this investigation would further disrupt solar projects, on June 6 President Joe Biden issued plans for a 24-month exemption from tariffs for solar panel imports from the four countries mentioned. This two-year break is intended to avoid stalling solar projects and will run parallel to the Department of Commerce investigation.

U.S. Renewable Capacity Additions