economy

April 6, 2026

Retail’s Private Credit Boom Is Flashing Warning Signs

About seven years ago, I received an unexpected outreach: A network of Ivy League alumni investors was inviting me to participate in a private credit deal. The pitch was polished and persuasive—access to “institutional-quality” investments, steady income and higher returns than what traditional portfolios could offer. It was the first time I seriously encountered private credit. And it immediately raised a question: Why was this being offered to me?

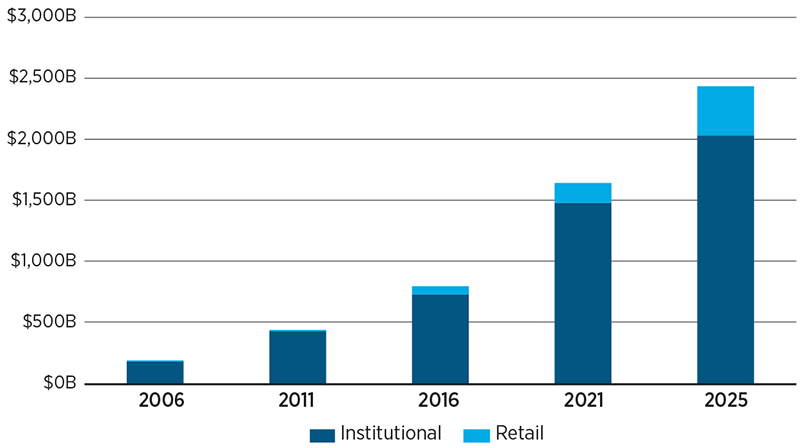

Over the past decade, retail participation in private capital has grown from negligible to a meaningful share of the market; now in double digits and still rising. This shift did not happen in a vacuum. It was born out of an extended period of near-zero interest rates that reshaped the entire investment landscape. For years, traditional assets offered little to no real return. The classic 60/40 portfolio no longer delivered what investors had come to expect. Retail investors noticed. And they asked questions.

Financial advisers were forced to respond. Telling clients to simply accept lower returns was not a viable answer. So portfolios were reallocated incrementally but systematically toward higher-yielding, less liquid alternatives. Private credit, with its promise of steady income and floating-rate protection, became a natural solution.

At the same time, private credit managers were facing pressures of their own. The asset class had grown rapidly, but its traditional capital base—pensions, endowments and sovereign funds—was reaching allocation limits. To sustain growth and fund an ever-expanding pipeline of loans, managers needed new sources of capital. Retail investors, representing a vast and largely untapped pool of wealth, became the marginal buyer. What emerged was not a coordinated plan, but a convergence: retail investors searching for yield, advisers under pressure to deliver it and private credit firms eager to supply it.

Now, early signs of strain are appearing. Redemption pressures are rising in retail-focused funds. Liquidity mismatches—between illiquid loans and semi-liquid fund structures—are being tested. Defaults are ticking up. Fraud has also been reported. Private credit is less regulated than public markets because it is meant for investors who are equipped to handle complexity and liquidity, such as institutional investors.

The expansion of retail into private credit was, in many ways, the price of cheap money. And as the cycle turns, we are beginning to see what that price may be.

Credit Institutional and Retail Fund Assets Under Management

SOURCE: PitchBook Global Private Debt Report.