- Main

-

Economists love averages. If you spend six months in a drought and six months in a flood, they'll report that rainfall was normal on average. A few years ago, a prominent economist argued that inflation's impact on households was overstated because wages had risen roughly as much as prices. On paper, the argument made sense. If incomes eventually catch up to inflation, then purchasing power should be largely preserved. However, households don’t live on cumulative statistics. They live on cash flow.

The flaw in the argument is that prices and wages do not move with the same timing or frequency. Grocery prices can rise multiple times within a year. Insurance premiums can jump at renewal. Gas prices can change daily. By contrast, most workers receive raises once a year, if at all. Even if wages eventually do catch up to inflation, families may spend months or years absorbing higher costs before their income adjusts. During that gap, they must find liquidity somewhere.

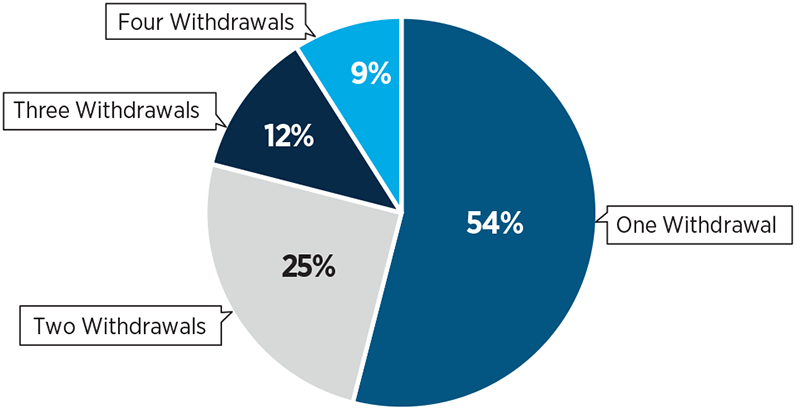

New data from Vanguard and the Federal Reserve Bank of New York illustrate this reality. Vanguard reports that a record 6% of 401(k) participants took hardship withdrawals in 2025. The largest uses were to avoid foreclosure or eviction and to pay medical expenses. Nearly half made multiple withdrawals. The median withdrawal was just $1,900, a revealing figure because a $1,900 withdrawal is not evidence of retirement failure, but of a cash-flow problem.

The New York Fed's data tells a similar story. Consumer delinquencies remain elevated, while mortgage distress has increased, most noticeably among lower-income households. These families are not necessarily insolvent. Many remain employed and continue contributing to retirement plans. Yet they increasingly struggle to bridge the gap between rising expenses and less frequently moving income. This helps explain an apparent contradiction in today's economy. Retirement balances are near record levels as retirement contribution rates are rising. Yet hardship withdrawals and delinquencies are also increasing.

The reason is simple: Wealth and liquidity are not the same thing. A household can have substantial home equity and a growing 401(k) and still lack enough cash to cover an unexpected medical bill or a rent increase. Our accountant friends understand this very well—financial health is not only the balance sheet but also the cash flow.

economy

June 22, 2026

Cash Flow Squeeze Forces Households To Pull from Retirement

Of Those Who Made Withdrawals,

Many Took Multiple Hardship Withdrawals

SOURCE: Vanguard Group, 2026 How America Saves.